Thursday, November 6, 2025

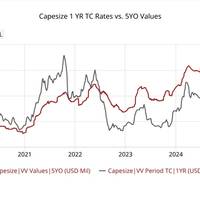

Capesize News

Sponsored Content

How Hot Is Your Cable? Understanding Subsea Cable Thermal Performance

Still trying to leverage digital in your operations? Create your own advantage

October 2025

Read the Magazine

Read the Magazine

Read the Magazine

This issue sponsored by:

Navigating the Limits: Columbia River Pilots Confront Big Ships, Tight Channels, and a Changing Maritime World

Subscribe for

Maritime Reporter E-News

Maritime Reporter E-News is the maritime industry's largest circulation and most authoritative ENews Service, delivered to your Email five times per week